Find your Next Fintech

Find your Next

Opportunity with SIASTES.

with SIASTES.

Fintech Opportunity

Connecting Top Talent with

the Best Fintech Companies Worldwide.

... explore our features

Job Search

Your Job Search Made Easier

with SIASTES

Your Job Search Made Easier

with SIASTES

5000 + Users

1000+ Available Jobs

We connect skilled

professionals from around the world with fintech

opportunities, ensuring fair pay and career growth for everyone.

Available on

App Store

Available on

App Store

Available on

App Store

Features

The New Era

of Job Search

4+ Features

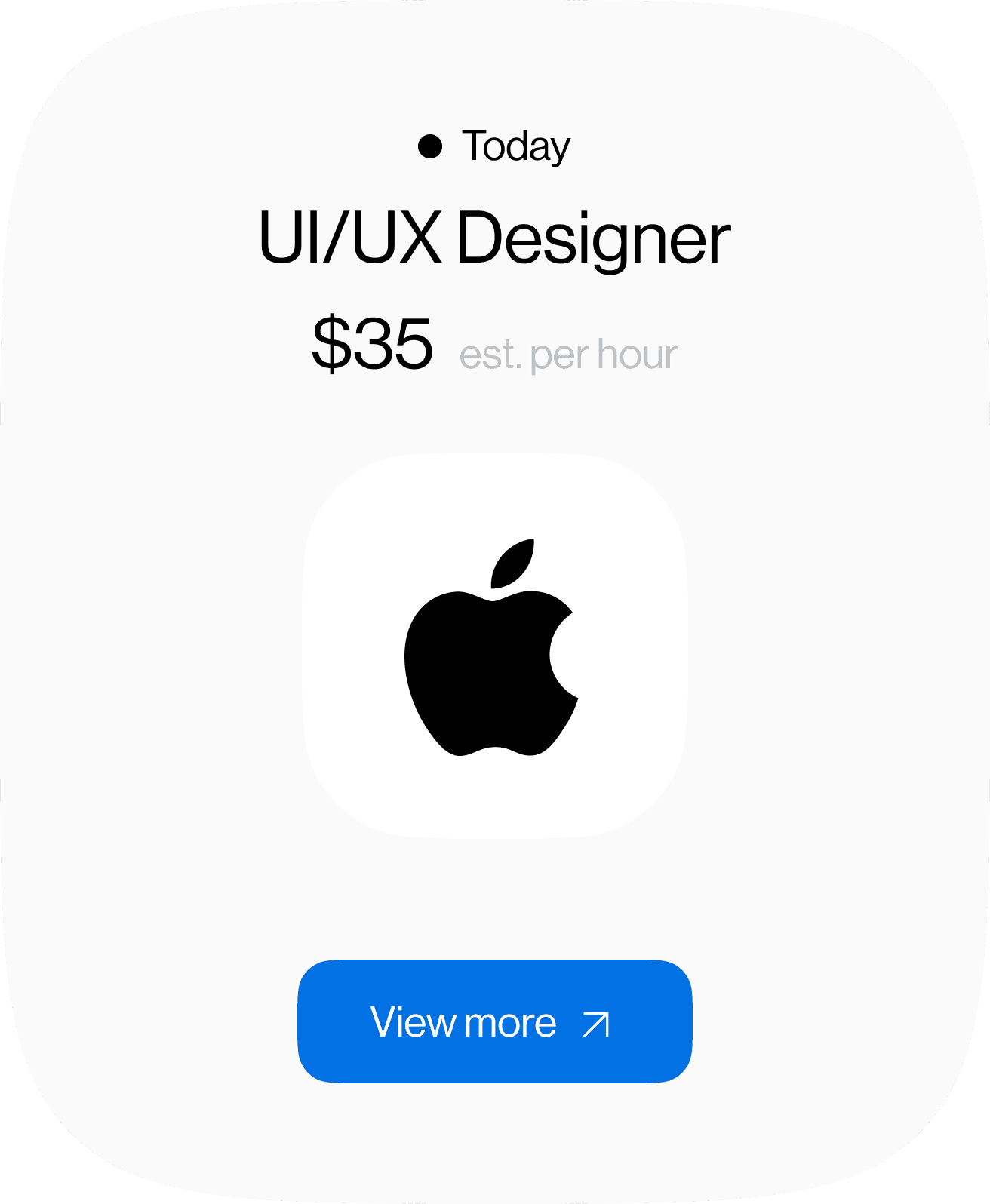

Latest Jobs

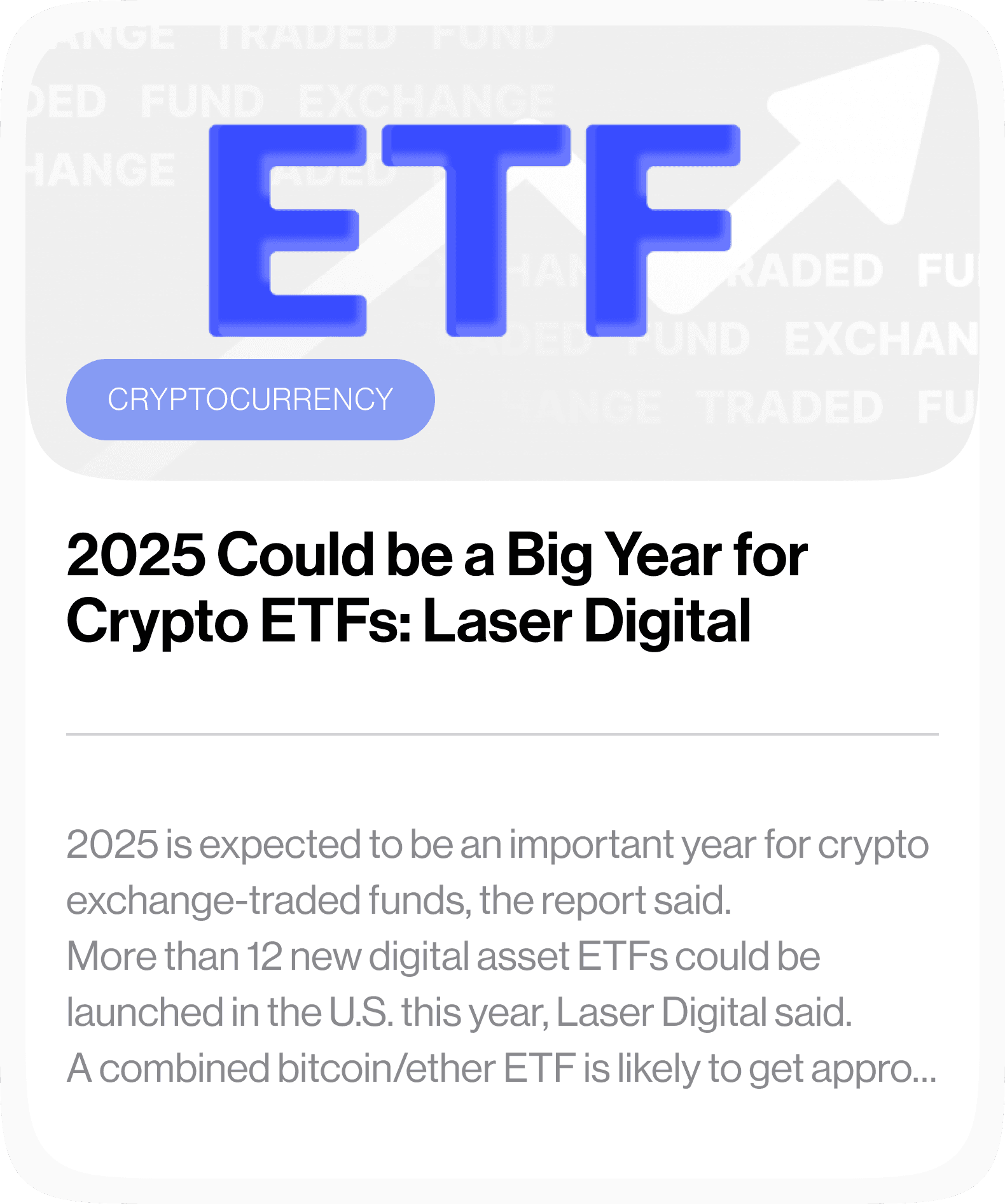

News

Social Chats

scroll down

Description

Find fintech job opportunities with our app. Whether you're experienced or new, we connect you with top companies. Explore roles that match your skills and take the next step in your career!

Stay updated with the latest job opportunities and industry news! Our app curates articles tailored to your career interests, helping you make informed decisions in your job search.

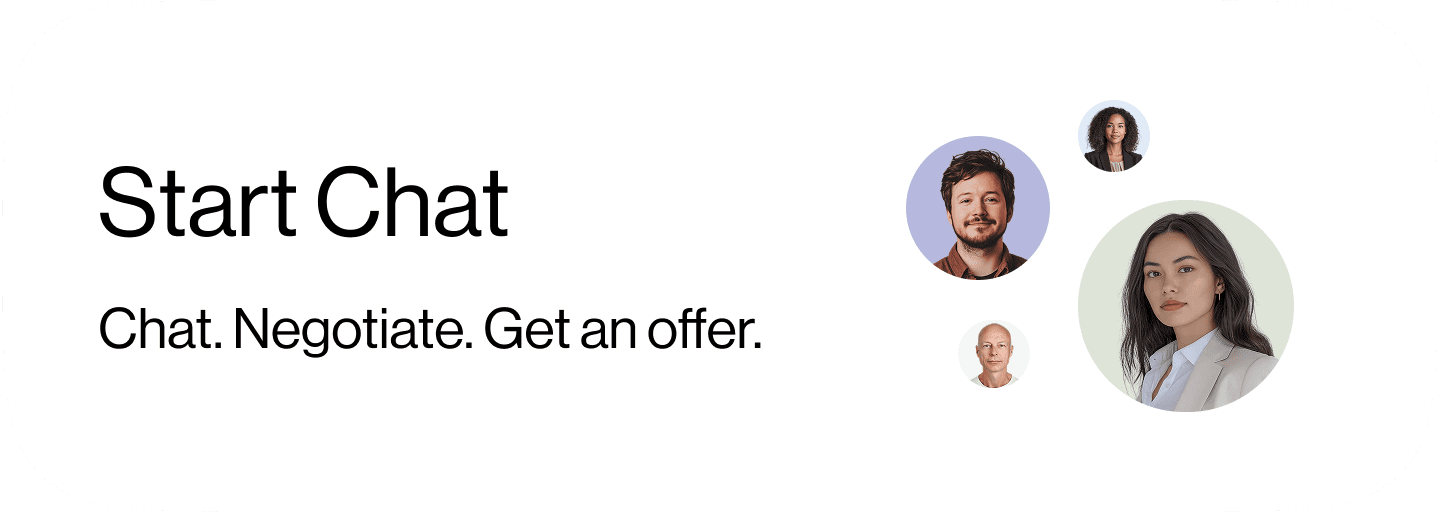

Connect with other job seekers in our 'Social Conversations' feature. Share tips, seek advice, and celebrate your successes together.

Find fintech job opportunities with our app. Whether you're experienced or new, we connect you with top companies. Explore roles that match your skills and take the next step in your career!

Stay updated with the latest job opportunities and industry news! Our app curates articles tailored to your career interests, helping you make informed decisions in your job search.

Connect with other job seekers in our 'Social Conversations' feature. Share tips, seek advice, and celebrate your successes together.

... our stats

Description

Social Chats

Connect with other job seekers in our 'Social Conversations' feature. Share tips, seek advice, and celebrate your successes together.

Description

Social Chats

Connect with other job seekers in our 'Social Conversations' feature. Share tips, seek advice, and celebrate your successes together.

Description

Social Chats

Connect with other job seekers in our 'Social Conversations' feature. Share tips, seek advice, and celebrate your successes together.

Description

News

Stay updated with the latest job opportunities and industry news! Our app curates articles tailored to your career interests, helping you make informed decisions in your job search.

Description

News

Stay updated with the latest job opportunities and industry news! Our app curates articles tailored to your career interests, helping you make informed decisions in your job search.

Description

News

Stay updated with the latest job opportunities and industry news! Our app curates articles tailored to your career interests, helping you make informed decisions in your job search.

Description

Latest Jobs

Find fintech job opportunities with our app. Whether you're experienced or new, we connect you with top companies. Explore roles that match your skills and take the next step in your career!

Description

Latest Jobs

Find fintech job opportunities with our app. Whether you're experienced or new, we connect you with top companies. Explore roles that match your skills and take the next step in your career!

Description

Latest Jobs

Find fintech job opportunities with our app. Whether you're experienced or new, we connect you with top companies. Explore roles that match your skills and take the next step in your career!

Stats

Numbers That Speak

Numbers

That Speak

10,000+

Active Jobs in Fintech

500+

Partner Companies

500+

Partner Companies

500+

Partner Companies

500+

Partner Companies

150,000+

Successful Hires

95%

User Satisfaction rate

Siastes Pay

Empowering the Diaspora

Arround the World to Get Paid

Empowering the Diaspora Arround the World to Get Paid.

Download the App

Find your Next

Fintech Opportunity

with SIASTES.

Download on the

App Store

Get in on

Google Play

Connecting Top Talent with the Best Fintech Companies Worldwide.

Download App

Product

App Store

Google Play Store

Get Updates

Subscribe to our newsletter

©2025 Siastes

Download the App

Find your Next

Fintech Opportunity

with SIASTES.

Download on the

App Store

Get in on

Google Play

Connecting Top Talent with the Best Fintech Companies Worldwide.

Download App

Product

App Store

Google Play Store

Get Updates

Subscribe to our newsletter

©2025 Siastes

Download the App

Find your Next

Fintech Opportunity

with SIASTES.

Download on the

App Store

Get in on

Google Play

Connecting Top Talent with

the Best Fintech Companies Worldwide.

Download App

Product

App Store

Google Play Store

Get Updates

Subscribe to our newsletter

©2025 Siastes

Download the App

Find your Next

Fintech Opportunity

with SIASTES.

Download on the

App Store

Get in on

Google Play

Connecting Top Talent with the Best Fintech Companies Worldwide.

Download App

Product

App Store

Google Play Store

Get Updates

Subscribe to our newsletter

©2025 Siastes